Key Takeaways

- Having a cheat sheet to the 2026 contribution limits gives you the context to make informed decisions about your financial future.

- Work with an accountant to make sure that each contribution is made correctly, and then talk with your financial advisor about how you can maximize your savings today for the goals you have in life.

Defined Contribution Plans (401ks, 403b, 457, TSP, etc.)

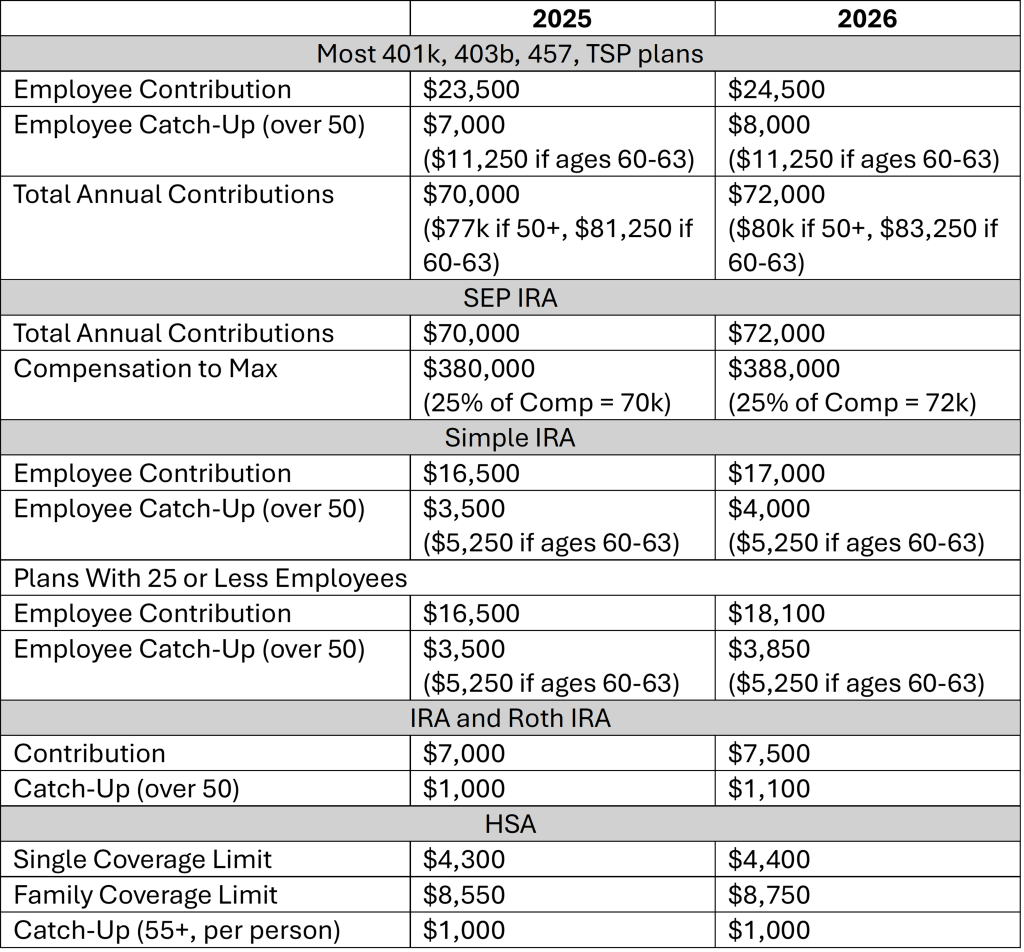

In 2025, those contributing to a company retirement account, like a 401k had certain contribution limits to stay within. For 401ks, the employee maximum contribution was $23,500 but increased to $24,500 in 2026. Historically, there has been a catch-up contribution available to earners over 50 years old. For 2025, the catch-up contribution was $7,000 and increased to $8,000 in 2026. Additionally, the Secure 2.0 Act created a “super catch-up” that started in 2025 for those aged 60 through 63. Those in this small age range could contribute an additional $11,250 instead of the “normal” $7,000 catch-up. For 2026, this additional amount will stay the same at $11,250.

For those looking to maximize their 401k contributions beyond just employee contributions, the total annual contribution limit rose in 2026 to $72,000 from $70,000 in 2025. This particularly applies to those making after-tax contributions to their 401k or those operating a Solo 401k plan. There is no explicit “employer” contribution limit; only that the sum of all contributions into one plan cannot exceed $72,000. The catch-up contributions do apply to this total limit as well, so in 2026, the limit for those over 50 is $80,000, and those 60-63 cap out at $83,250.

“Company” Individual Retirement Accounts (SEP IRAs, Simple IRAs)

SEP IRA contributions are not necessarily based on a contribution limit, but rather up to 25% of the eligible compensation for the year. SEP IRAs do limit contributions at the same annual contribution maximum as 401k plans. For 2025, that cap was $70,000, and in 2026 it will be $72,000. SEP contributions are generally allowed for the previous year, up until tax returns are filed.

Employee contributions to a Simple IRA were capped at $16,500 in 2025 and increased to $17,000 in 2026. Interestingly, Simple IRA plans with 25 or fewer employees can contribute more, starting in 2026. Employees at these companies can contribute $18,100, with a $3,850 catch-up for those over 50 (and the same $5,250 for those 60-63). Employer contributions are generally capped at 2-3% of the employee’s compensation, so the total contribution is not terribly relevant for Simple IRAs.

“Personal” Individual Retirement Accounts (IRAs and Roth IRAs)

In 2025, those with enough earned income can also contribute $7,000 to either an IRA or a Roth IRA. Those over 50 could contribute an additional $1,000. In 2026, the contribution limit was raised to $7,500 between IRAs and Roth’s, with a catch-up contribution of $1,100. Technically, these contributions can be made up to the date you file your taxes the following year. For example, those who have not made a 2025 contribution to a Roth IRA by January 2026 could contribute $7,000 for 2025 and another $7,500 for 2026, totaling $14,500.

These contributions are made to individual accounts that are not tied to any company. However, the presence of another “company” retirement account could impact the contributions. For Traditional IRAs, there are phaseout rules to remove the tax deduction if your income gets too high. Depending on whether a professional and/or their spouse has access to a company plan, and how much total income they have, it will factor into whether they can deduct the $7,500 in 2026.

Roth IRAs have a similar requirement, but only related to the income of the household, and not a company retirement plan. In 2026, single filers making over $168,000 and married couples making over $252,000 cannot contribute to a Roth IRA. This is separate from any Roth 401k contribution, which generally doesn’t have any income restrictions.

Health Savings Accounts (HSAs)

HSA contributions for 2025 were limited based on the healthcare plan you are enrolled in. For those with single coverage, the contribution limit increased in 2026 to $4,400 from $4,300. For those with family coverage, the limit increased to $8,750 from $8,550. There is a catch-up contribution of $1,000 for those over 55 years old.

To qualify for an HSA, health plans must also meet deductible and maximum out-of-pocket limits. For 2025, the deductible had to be at least $1,650 ($3,300 family coverage). In 2026, those limits increased to $1,700 ($3,700 family). For 2025, the maximum out-of-pocket limits could not exceed $8,300 ($16,600 for a family). This limit increased to $8,500 ($17,000 family) in 2026.

New Year, New Rules

As usual, tax planning and retirement planning are a moving goalpost. The goal is not to memorize every deduction and limit, but to have the context to make informed decisions about your financial future. Work with an accountant to make sure that each contribution is made correctly, and then talk with your financial advisor about how you can maximize your savings today for the goals you have in life. Contributions to retirement accounts are one piece of a larger puzzle. Take the time to understand why you are contributing to your accounts and what the best strategy is to accomplish your plans.